Civil Engineering Reference

In-Depth Information

In (

5

), f

ij

is the frequency of being in state i and transit to state j. The transition

matrix P is computed just by counting each state frequency and dividing that by

the total amount of transitions (Ching and Ng

2005

).

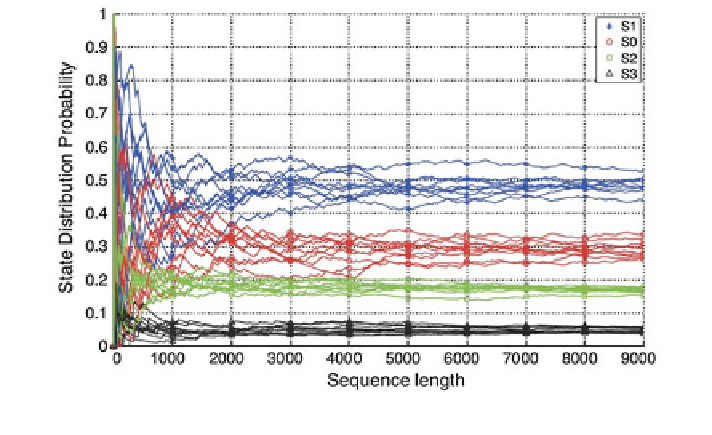

3.5 Model Validation

The validation process takes advantage of the stationarity of the ECM stochastic

model. This implies that its statistical characteristics do not change over time. That

is, the provided time series varies over time; however, its characteristics such as

mean and variance converge to constant values. The cumulative state distribution

over a finite horizon for a MC similar to the one in Fig.

7

a is depicted in Fig.

8

.

Since the model is stochastic, the generated sequences in Fig.

7

b, also referred as

time series or paths, are different. However, with this model structure, the state

probability distribution converges to a stationary distribution also referred as

steady state distribution (Pollard

1984

). The steady-state distribution is a charac-

teristic of the model and not of the generated sequence. Generally, there are two

ways of determining the steady-state distribution, either by simulation or by

analytically. The simulation method consists in generating a sequence with the

model over a sufficient large period. Next, the generated sequence is analysed, and

the state distribution is computed. The problem is to define how large should the

period be for the different models. The analytical method uses the time-homo-

geneous property of the MC as follows:

Fig. 8

Simulation of a Markov chain with 4 states over different initial conditions