Database Reference

In-Depth Information

for all

Thus, a particular point in the time series can be expressed as a linear combination

of the prior p values, for j = 1, 2, …p, of the time series plus a random

error term, . In this definition, the time series is often called a

white noise

process

and is used to represent random, independent fluctuations that are part

of the time series.

From the earlier example in

Figure 8.3

,

the autocorrelations are quite high for

the first several lags. Although it appears that an AR(8) model might be a good

candidate to consider for the given dataset, examining an AR(1) model provides

further insight into the ACF and the appropriate value of p to choose. For an AR(1)

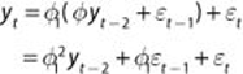

model, centered around

,

Equation 8.5

simplifies to

Equation 8.6

.

Based on

Equation 8.6

, it is evident that

. Thus, substituting

for

yields

Equation 8.7

.

Therefore, in a time series that follows an AR(1) model, considerable

autocorrelation is expected at lag 2. As this substitution process is repeated,

can be expressed as a function of for …and a sum of the error

terms. This observation means that even in the simple AR(1) model, there will be

considerable autocorrelation with the larger lags even though those lags are not

explicitly included in the model. What is needed is a measure of the autocorrelation

between for h = 1, 2, 3… with the effect of the values

excluded from the measure. The

partial autocorrelation function (PACF)

provides such a measure and is expressed as shown in

Equation 8.8

.

where