Information Technology Reference

In-Depth Information

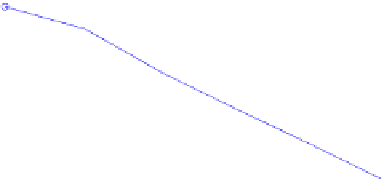

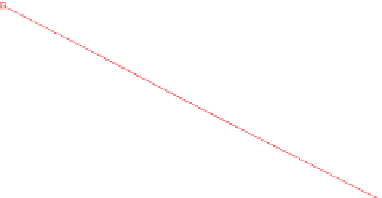

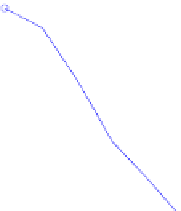

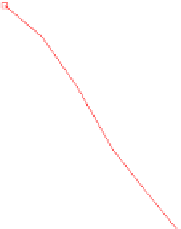

Fig. 15.2

Convergence rate

of the one-factor (

top

)and

two-factor (

bottom

) Bates

model on sparse tensor

product space

15.5 Further Reading

A stochastic volatility model with jumps comparable to the BNS model is the so-

called COGARCH(1

,

1) process introduced by Klüppelberg et al. [105]. This model

is a continuous time version of the popular GARCH model in discrete time and

states that the asset log-price

X

is given by d

X

t

=

σ

t

d

L

t

, where

L

is a Lévy pro-

cess and the jumps

L

of this Lévy process are also used to define the volatility

process

σ

. The model is generalized to the COGARCH(

p,q

) process by Brockwell

et al. [30].

A large class of stochastic volatility models is described by Carr et al. [37] where

the stock price process

S

is given as the ordinary or the stochastic exponential of a

stochastic volatility process

Z

t

=

L

Y

t

, which is obtained by subordinating a Lévy

process

L

to

Y

(which, for example, is given by the CIR model).

Search WWH ::

Custom Search