Information Technology Reference

In-Depth Information

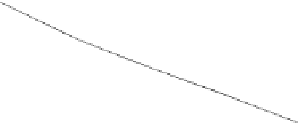

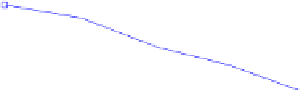

Fig. 15.3

To p

: Convergence

rate of price

u(ρ

0

)

and

sensitivity

u(δρ)

for

IG(

a,b

)-OU BNS model.

Bottom

: Computed sensitivity

u(δρ)

for IG(

a,b

)-OU

More recent works consider multivariate stochastic volatility models, where the

SV models for one underlying are extended to

d>

1 assets. In such models, the

matrix

Σ

in (8.1) is defined, for example, as the solution of a matrix-valued SDE

both without and with jumps. We refer to, e.g. Cuchiero et al. [48], Dimitroff et al.

[58], Muhle-Karbe et al. [127] and the references therein.

Search WWH ::

Custom Search