Environmental Engineering Reference

In-Depth Information

4

2

0

x

n

−

2

−

4

0

128

256

384

512

n

(a)

40

20

0

x

n

−

20

−

40

0

128

256

384

512

n

(b)

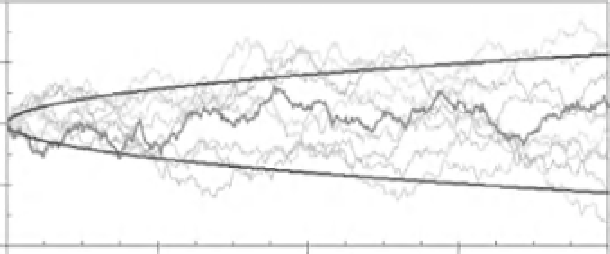

40

Figure 3.4

White noise and Brownian

motions. (a) An example of a Gaussian

white noise. Successive values are chosen

randomly from a Gaussian distribution

(

E

quation 3.2, Figure 3.2) with zero mean

(

x

=

0

.

0) and unit variance (

σ

20

0

x

n

x

=

1

.

0).

Adjacent values are not correlated. (b) The

white noise in (a) is summed using

Equation 3.4 to give a Brownian motion.

(c) Twelve examples of Brownian motions

are superimposed, each constructed from a

white noise. The envelope (solid parabolic

line) gives the standard deviation after

n

steps (Equation 3.5).

−

20

−

40

0

128

256

384

512

n

(c)

We have shown how an uncorrelated time series can

be created with a Gaussian distribution of values. How-

ever, the Gaussian distribution has limitations, including

the fact that the distribution is symmetric and values

are specified over the range

−∞

<

x

n

<

∞

. Many time

series have frequency-size distributions that are heavily

asymmetric and/or are restricted to only positive values.

All five real-world time series given in Figure 3.1 have

positive values only, with just two of the examples show-

ing (some) symmetry in the frequency-size distributions.

There are many other statistical distributions used to

model time series, with just one example of a widely

used one for positive values (and asymmetry) being the

log-normal distribution.

Search WWH ::

Custom Search