Environmental Engineering Reference

In-Depth Information

1.6.2 CDF transform approach

Let (Y

1

, Y

2

, …, Y

d

) denote multivariate non-normally distributed random variables. One

well-known CDF transform approach for constructing a valid multivariate distribution for

these random variables is

1. Define

=

()

X

Φ

1

F Y

(1.100)

i

i

i

where Φ

−1

(⋅) = inverse standard normal CDF and Fi(⋅)

i

(⋅) = CDF of Yi.

i

. By definition, (X

1

,

X

2

, …, X

d

) are

individually

standard normal random variables. That is, the histogram

of any component, Xi,

i

, will look normal (bell-shaped).

2. Assume (X

1

, X

2

, …, X

d

) follows a multivariate standard normal distribution as defined

necessarily follow a multivariate standard normal distribution even if each component

is standard normal. For example, if the scatter plot of Xi

i

versus X

j

shows a distinct

nonlinear trend, then the multivariate normal distribution assumption is incorrect.

You can apply the Mahalanobis distance test in Section 1.4.3 as well. The entries in the

correlation matrix

C

in

Equation 1.56

are the Pearson moment-product correlations

among (X

1

, X

2

, …, X

d

). Recall that for multivariate standard normal (X

1

, X

2

, …, X

d

),

the Pearson and Spearman (rank) correlations are nearly identical. Together with the

fact that the rank correlation between (Xi,

i

, X

j

) is identical to that between (Yi,

i

, Y

j

), the

entries in

C

are nearly the same as the rank correlations among (Y

1

, Y

2

, …, Y

d

).

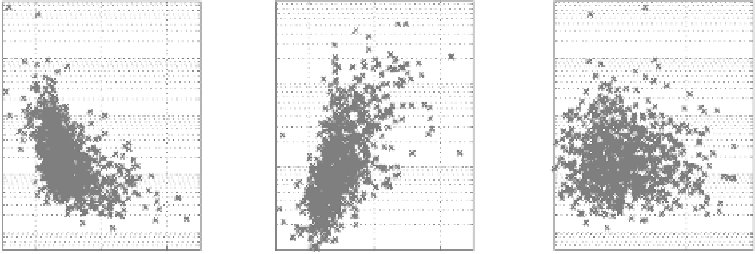

1.6.3 estimation of the marginal distribution of Y

These 1000 data points have full multivariate information: each data point has known (Y

1

,

Y

2

, Y

3

) values. In contrast, incomplete multivariate information will contain data points

such as (Y

1

, Y

2

, ?), (Y

1

, ?, Y

3

), and (?, Y

2

, Y

3

). The question marks denote unknown values.

The treatment of incomplete multivariate information is presented in Section 1.7. The mul-

tivariate data points are simulated using the procedure discussed in Section 1.6.5, with the

10

3

10

3

10

3

10

2

10

2

10

2

10

1

10

1

10

1

10

0

10

0

10

-1

10

-1

10

0

0

2

Y

1

= LI

4

0

2

Y

1

= LI

4

10

0

10

2

exp(Y

3

) =

S

t

Figure 1.25

Simulated multivariate datasets for non-normal (Y

1

, Y

2

, Y

3

).

Search WWH ::

Custom Search