Database Reference

In-Depth Information

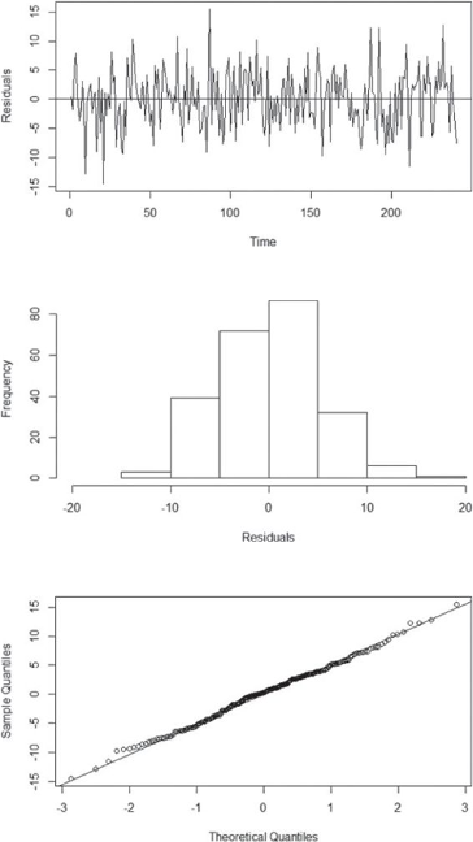

If the normality or the constant variance assumptions do not appear to be true, it

may be necessary to transform the time series prior to fitting the ARIMA model. A

common transformation is to apply a logarithm function.