Database Reference

In-Depth Information

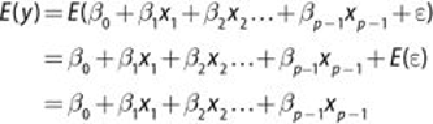

6.4

where:

is the outcome variable

are the input variables, for j = 1, 2,…, p - 1

is the value of

when each

equals zero

is the change in

based on a unit change in

, for j = 1, 2,…, p - 1

and the

are independent of each other

This additional assumption yields the following result about the expected value of

y, E(y) for given

:

Because

are constants, the E(y) is the value of the linear regression

model for the given

. Furthermore, the variance of y, V(y), for given

is this:

Thus, for a given , y is normally distributed with mean

and variance . For a regression model with

just one input variable,

Figure 6.3

illustrates the normality assumption on the error

terms and the effect on the outcome variable, , for a given value of .