Geoscience Reference

In-Depth Information

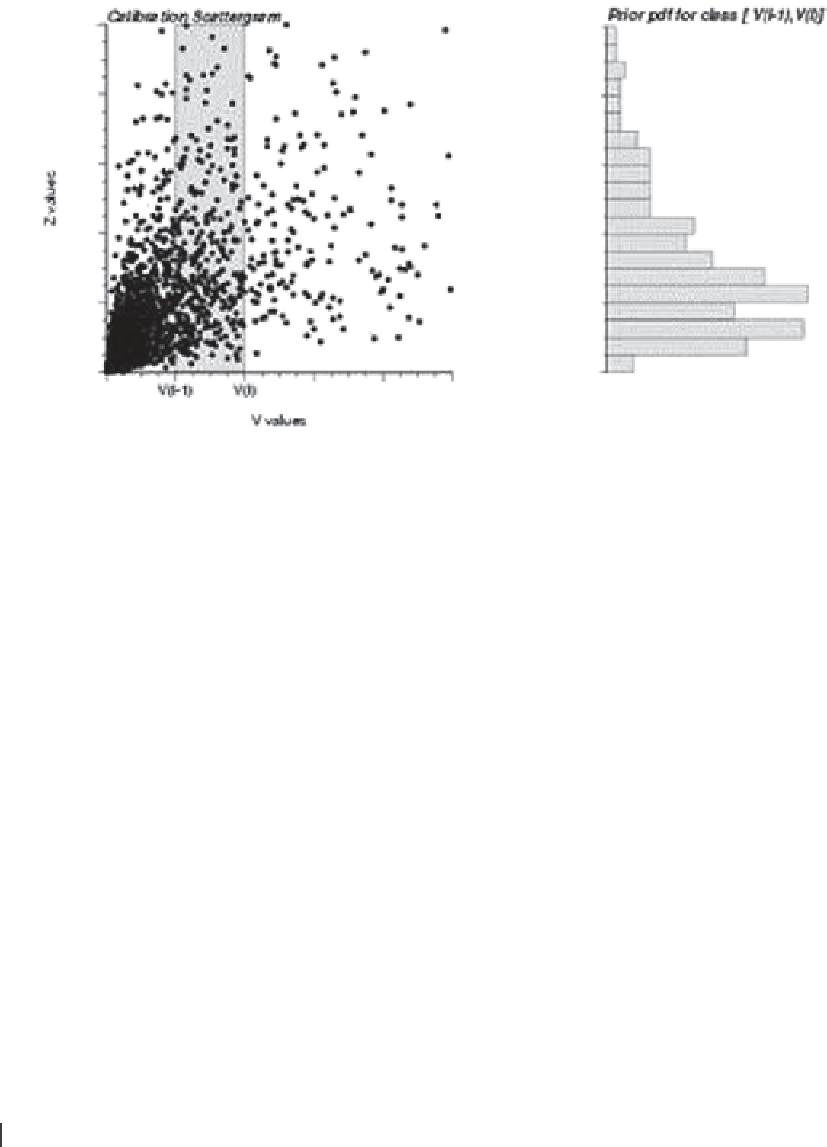

Fig. 10.15

Inference of the

soft prior probabilities from a

calibration scattergram. The prior

z probability pdf at a location

u′

α

where the secondary variable is

v(

u′

α

) in (v

l−1

, v

l

] is identified to

the calibration conditional pdf,

shown in the right of the figure

soft y indicator spatial distribution is likely different from

that of the hard i indicator data:

Consider a calibration data set {y(

u

α

; z), i(

u

α

; z), α = 1,…,n}

where the soft probabilities y(

u

α

; z) valued in [0,1] are com-

pared to the actual hard values i(

u

α

; z) valued 0 or 1. m

(1)

(z)

is the mean of the y values corresponding to i = 1; the best

situation is when m

(1)

(z) = 1, that is, when all y values exactly

predict the outcome i = 1. Similarly, m

(0)

(z) is the mean of the

y values corresponding to i = 0, best being when m

(0)

(z) = 0.

The parameter B(z) measures how well the soft y data

separate the two actual cases i = 1 and i = 0. The best case is

when B(z) = ± 1, and the worst case is when B(z) = 0; that is,

m

(1)

(z) = m

(0)

(z).

The case B(z) = − 1 corresponds to soft data predictably

wrong and is best handled by correcting the wrong probabili-

ties y(

u

α

; z) into 1 − y(

u

α

; z).

When B(z) = 1, the soft prior probability data y(

u

α

; z) are

treated as hard indicator data and are not updated. Converse-

ly, when B(z) = 0, the soft data y(

u

α

; z) are ignored; i.e., their

weights become zero.

Since the Y covariance model generally presents a

strong nugget effect, the Markov model implies that the

y data have little redundancy with one another. The un-

desired effect of this is that too much weight is given to

clustered, mutually redundant y data. In practice, only the

closest y datum is retained, which leads to using the col-

located correlation, i.e., the soft autocovariance at distance

0, C

Y

(h =

0

; z).

C zC

(;)

h

≠

(;)

h

zC z

≠

(;)

h

Y

IY

I

Then the indicator cokriging amounts to a full updating of all

prior cdf's that are not already hard.

At the location of a constraint interval j(

u

α

; z), indicator

kriging or cokriging amounts to in-filling the interval (a

α

, b

α

]

with spatially interpolated ccdf values. Thus if simulation

is performed at that location, a z attribute value would be

drawn necessarily from within the interval.

10.6.2

Markov-Bayes Model

With enough data one could infer directly and model the

matrix of covariance functions (one for each cutoff z):

[C

Y

(

h

; z) ≠ C

IY

(

h

; z) ≠ C

I

(

h

; z)]. An alternative to this te-

dious exercise is provided by the Markov-Bayes model,

whereby:

C

(;)

h

z

=

BzC

() (;),

h

z

∀

h

IY

I

2

C

(;)

h

z

=

B zC

() (;),

h

z

∀>

h

0

Y

I

=

Bz C

( )

( ;

h

z h

),

=

0

I

The coefficients B(z) are obtained from calibration of the

soft y data to the hard z data:

10.6.3

Soft Data Calibration

Consider the case of a primary continuous variable z(

u

) in-

formed by a related secondary variable v(

u

). The series of

hard indicator data valued 0 or 1, i(

u

α

; z

k

), k = 1,…,K, are

derived from each hard datum value z(

u

α

).

The soft indicator data, y(

u

α

,z

k

) in [0,1], k = 1,…,K, cor-

responding to the secondary variable value v(

u

α

), can be

(1)

( 0 )

Bz

()

=

m

()

z

−

m

() [1, 1]

z

∈− +

with:

m

(1)

()

z

=

EY

{(;) (;) 1}

u

z I

u

z

=

m

(0)

()

z

=

EY

{(;) (;) 0}

u

z I

u

z

=