Information Technology Reference

In-Depth Information

11

10

9

8

7

6

5

4

3

6000

0

1000

2000

3000

Day

4000

5000

(2 Jan 75)

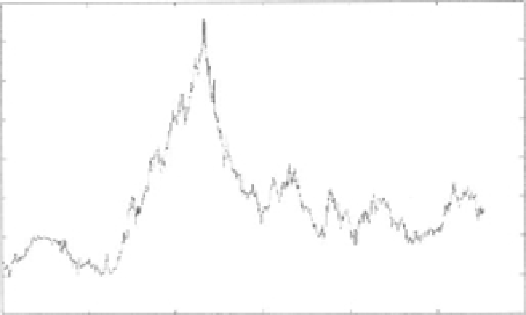

Figure 4.6.

The time series for the FRF/USD currency exchange time series from 1/2/75 to 1/15/99 with a

total of 5,529 data points [

36

]. Reproduced with permission.

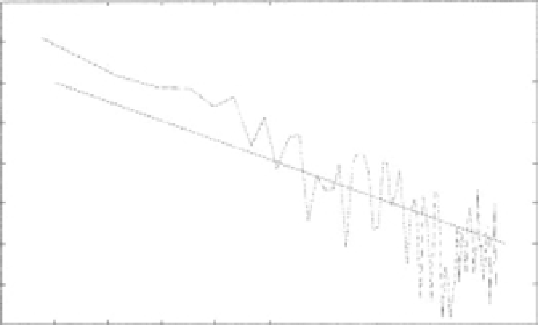

10

8

6

4

Slope

=

-2.8567

2

0

-2

-4

-6

-9

-6

-5.5

-5

-4.5

-4

-8.5

-8

-7.5

-7

-6.5

log

|λ|

The power spectral density for the FRF/USD currency exchange time series from 1/2/75 to

1/15/99 with a slope of -2.86 and a corresponding Hurst exponent of

H

=

0

.

93 [

36

].

Reproduced with permission.

Figure 4.7.

such as that shown in Figure

4.6

, which is a combination of short-time variations and

long-time excursions.

The typical financial time series in Figure

4.6

gives rise to the inverse power-law

spectral density shown in Figure

4.7

. The best fit to the individual slopes of the spec-

tra lies in the interval

−

2

.

86

≤

slope

≤−

2

.

11. The individual slopes are associated

with

−

(

2

H

+

1

)

in the spectral density, so the Hurst parameter lies in the inter-

val 0

Pesee argues that since the Hurst indices for JPY/USD and

EUR/USD approach 0.5 there is no memory in these cases and these financial time

series can be represented by standard random walks, similarly to the observation made

by Bachelier. On the other hand, there is clear evidence of the long-time memory for

.

55

≤

H

≤

0

.

93

.