Information Technology Reference

In-Depth Information

1

0.85

0.95

0.8

0.9

0.75

0.85

0.7

0.8

0.65

0.75

0.7

0.6

0.65

0.55

0.6

0.5

0.55

0.45

0.5

0

2

4

6

8

10

x 10

4

1.95

2

2.05

2.1

2.15

2.2

t

t

x 10

4

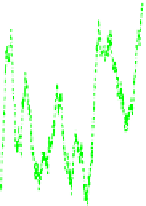

Fig. 5.

The time evolution of

Ψ

(

t

)(left)and

Ψ

(

t

) calculated in sliding window of

length equal to 100 (right) for

λ

-GCMG with

N

=1,

λ

=0

.

97 and strategies from

RSS. Red solid line corresponds to

m

= 1, dashed blue line corresponds to

m

=2,

green dashed-dotted line corresponds to

m

= 5. The predicted signal is FW20.

utility than the basic ones correctly recognizing shorter patterns. This happens

randomly, as sometimes samples are in order that is reflected by some of addi-

tional strategies. However, the pattern does not truly exist. In the next steps the

forecast, based on one of additional strategies, is mostly wrong, what lowers the

correctness. In other words, too long memory spoils the predictor introducing

noise of unwanted strategies. The observed degradation of correctness for longer

m

indicates that there are no long-range and complicated patterns in the signal

or that their nature is more subtle than MG strategies are able to capture. The

first statement is supported by observations of the autocorrelation of returns,

where the only distinct value is for

τ

= 1. Similar premise is also included in

Ref. [12].

The success rate for

m

=1,itismostlyabove0

.

6, and from time to time

even touches the level 0

.

8, if calculated in the sliding window. The mean value

of correctness is 0

.

7 (Fig. 5 - left), what seems impressive, at the first sight.

However, we checked that the correctness of the linear regression model of the

first order is equal to 0

.

68. The use of higher-order filters does not improve the

predictor.

The next question is, whether the results achieved for FW20 are specific only

for this asset or they are more universal. We examined separately 5 stocks with

the biggest impact on FW20 index (Fig. 6). The success rate decreases as a

function of

m

, regardless of the analyzed year. So the results seem to be time

and stock independent.

Another interesting issue is related to the analysis of the best strategy. The

question is, whether there is only one strategy permanently outperforming other

strategies or, maybe, different strategies lead at various moments? If there is only

one, it would mean that patterns do not change over the game or that they do in

a way the strategies are unable to capture. One permanently best strategy also

would mean that the extended adaptive version of algorithm is, at least in this