Agriculture Reference

In-Depth Information

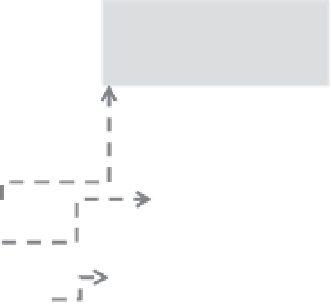

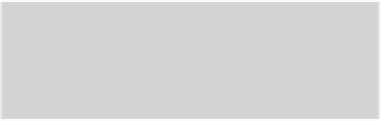

Land management

projects for enhanced C

storage

Satellite imagery interpreted for land

cover change, with known accuracy and

legend matching C data sets and activity

data

National account-

ability for appro-

priate mitigation

actions

See Fig. 31.2 for

further linkages

Area-based

accounting

(national,

subnational

or 'project'

level)

Management infor-

mation on land-use

systems: life-cycle,

drainage, fertilization

Good management

practice certification

for international trade

Fig. 31.5.

Area-based and trade-based interventions to reduce net emissions from land use (change)

interact with the national accounting frame (compare

Fig. 31.2)

and accountability vis-à-vis nationally

appropriate mitigation actions.

argument to include all soils, to avoid the

type of definitional confusion that has con-

siderably slowed down REDD efforts.

The IPCC AFOLU accounting frame-

works require that changes in soil carbon

stocks across all land uses are part of a

5-

yearly (non-Annex-I) or annual (Annex-I)

reporting cycle at the national scale. Is there

scope for monitoring at subnational or 'pro-

ject' scales as well?

Table 31.2

summarizes

the pros and cons of the argument.

concern that cannot be addressed easily

without new research.

The integrity of the accounting sys-

tem is challenged by cross-border trade,

especially where this involves Annex-I and

non-Annex-I countries. Long-term stock

change is the primary accounting base

for terrestrial carbon and has a diminish-

ing cumulative error, as overestimates of

change for a single period tend to be com-

pensated by underestimates for a subse-

quent period. Flow accounting errors do

not diminish by accumulation, and cumu-

lative trade estimates need to be reconciled

with the stock changes they lead to. There

is, however, little reason to treat carbon in

internationally traded wood differently

from carbon in other organic produce, be it

used as animal feed, human food and fibre,

or as a source of bioenergy (van Noordwijk

et al

., 1997). The inclusion of international

trade in wood and wood products in car-

bon accounting has long been debated

(Winjum

et al

., 1998). If implemented, it al-

lows wood-exporting countries to claim

carbon sequestration - but the consequent

emissions in importing countries are pref-

erably ignored. Lauk

et al

. (2012) con-

cluded that increments from 1900 to 2008

in the carbon stocks held in wood and

Integrity of accounting rules

Spatial aggregation shifts determinants of

uncertainty in soil C stocks in ways that

are poorly recognized as yet (Lusiana

et al

.,

2013). The confidence intervals around

national estimates of net soil C change are

much narrower than those at project level,

due to the number of the at least partially

independent replicates involved. The ag-

gregate numbers mostly suffer from pos-

sible bias, rather than random error. Biases

inherent in the availability of data that are

not derived from stratified random de-

signs, but depend on whatever has been

collected for other reasons, are a major

Search WWH ::

Custom Search