Information Technology Reference

In-Depth Information

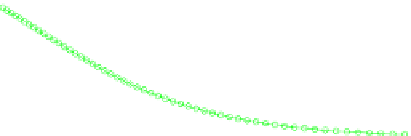

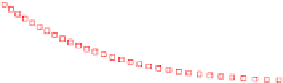

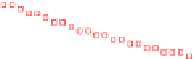

Fig. 6.4

Swing option prices

(

top

) and corresponding

exercise boundary (

bottom

)

6.5 Further Reading

Pricing of barrier options goes back to Merton [124]. In the recent paper from

Zvan [167], an overview over various computational methods is given. Similar

partial differential equation formulations for the Asian options are given in Inger-

soll [91], Rogers and Shi [142]. A unifying approach is presented by Vecer [157].

Compound options were studied by Geske [69] where also a closed form solution

was given. Obtaining swing option prices using a finite difference method was con-

sidered in Dahlgren [49] and for finite elements in Wilhelm and Winter [160].

Search WWH ::

Custom Search