Information Technology Reference

In-Depth Information

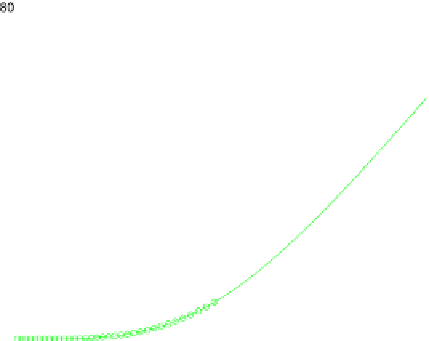

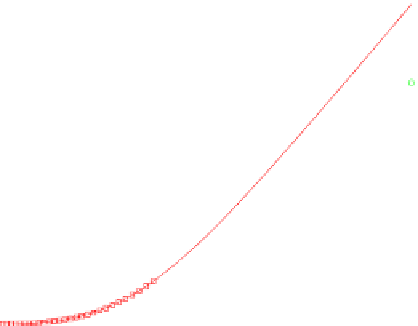

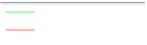

Fig. 6.3

Compound call and

underlying call option

We obtain the result by applying Theorem 4.3.1 to

v

R

,

|

|

≤

|

|

+

|

|

v(t,x)

−

v

R

(t, x)

v(t,x)

−

v

R

(t, x)

v

R

(t, x)

−

v

R

(t, x)

≤

C

4

(T , σ ) e

−

γ

5

R

+

γ

6

|

x

|

+

C

3

(T , T

1

,σ)e

−

γ

3

R

+

γ

4

|

x

|

,

where the option price

v

1

satisfies (4.10) since

g

1

satisfies (4.10).

Therefore, we have the weak formulation on the bounded domain

G

and in time-

to-maturity

Find

u

∈

L

2

((

0

,T)

;

H

0

(G))

∩

H

1

((

0

,T)

;

L

2

(G))

such that

(∂

t

u, v)

a

BS

(u, v)

H

0

(G),

a.e. in

(

0

,T)

+

=

0

,

∀

v

∈

u(

0

)

=

g(u

1

(T

1

−

T )),

where the underlying option price

u

1

satisfies

L

2

((

0

,T

1

−

H

0

(G))

H

1

((

0

,T

1

−

L

2

(G))

such that

Find

u

1

∈

T)

;

∩

T)

;

a

BS

(u

1

,v)

H

0

(G),

a.e. in

(

0

,T

1

−

+

=

∀

∈

(∂

t

u

1

,v)

0

,

v

T)

g

1

(e

x

)

u

1

(

0

)

=

|

G

.

Example 6.3.2

Consider a compound call option in a Black-Scholes market. Set

K

1

=

0

.

01. We plot the price of

the compound options and the corresponding underlying call price in Fig.

6.3

where

we used finite elements for the discretization. It can be seen that the price of the

compound option is lower than the price of the underlying option.

100,

K

=

20,

T

1

=

1,

T

=

0

.

5,

σ

=

0

.

3 and

r

=

Search WWH ::

Custom Search