Information Technology Reference

In-Depth Information

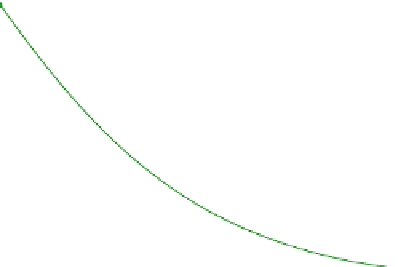

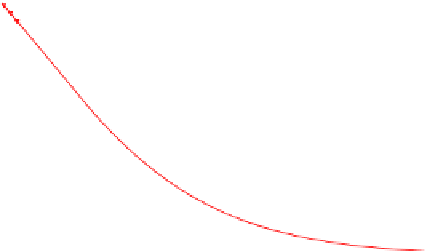

Fig. 16.4

Option prices for

several models for a

European put option with

T

=

1and

K

=

100

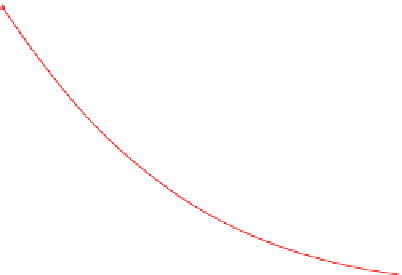

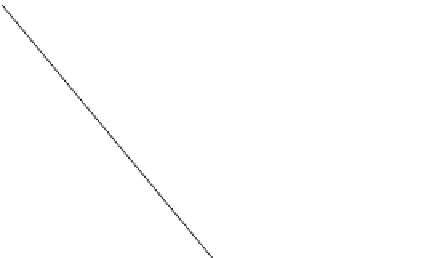

Fig. 16.5

Option prices for

several models for an

American put option with

T

=

1and

K

=

100

16.7 Further Reading

Schneider et al. [137] consider the well-posedness and discretization of pricing

equations on variable order spaces. For the multidimensional setting we refer to

Reichmann and Schwab [138] and Reichmann [135]. Extensions of Lévy type mar-

ket models involving local speed functions have also been considered by Carr et

al. [35]. A generalized NIG model was proposed by Barndorff-Nielsen and Leven-

dorski

ˇ

i[7].

Search WWH ::

Custom Search