Environmental Engineering Reference

In-Depth Information

Table 1

Volatility estimates

Commodity

With drift

a

Without drift

Crude oil cushing, OK WTI

0.2847

0.2840

New York harbor conventional gasoline

0.3090

0.3082

New York harbor ultra-low sulfur No. 2 diesel

0.2311

0.2305

a

The drift is the deterministic part of the differential equation. Before the volatility is calculated,

the effect of the deterministic trend should be eliminated, but in practice that effect is often very

small and volatility can be calculated without this prior adjustment

reversion, using the IGBM differential equation, the following estimate can be

drawn up:

S

t

þ r

D

p

e

t

S

t

þ

1

S

t

S

t

¼

k

D

t þ kS

m

D

t

1

ð

11

Þ

and with the residues of the differential equation the volatility levels can be esti-

mated, resulting in the

gures shown in the third column of Table

1

.

As can be seen, in this case the differences are minimal, given that the drift for a

small

D

t

has very little effect.

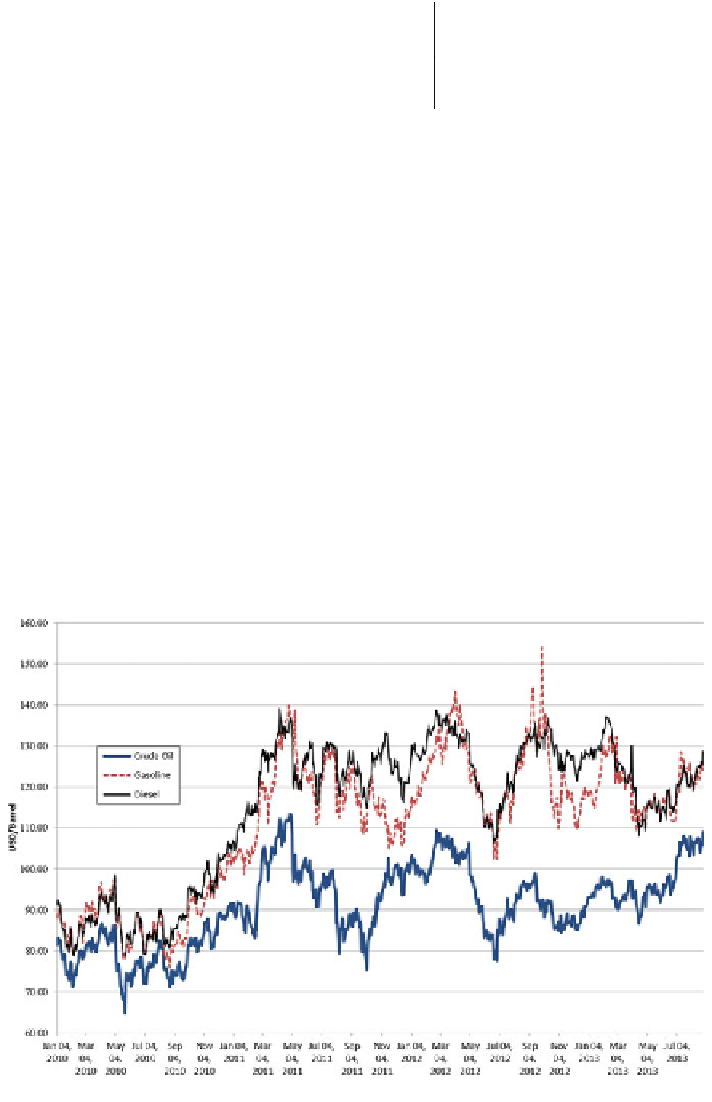

Figure

1

, calculated using the same data source, shows the historical trend in the

prices of the commodities in Table

1

:

Fig. 1

Historical spot prices of Crude Oil, Gasoline and Diesel

Search WWH ::

Custom Search