Environmental Engineering Reference

In-Depth Information

25

20

Lignocell.

15

($3/GJ)

10

Starch

Nat.

gas

($5/GJ)

Ve g.

oil

5

$75/bbl

$25

($1/GJ)

Crude oil

($15/GJ)

0

0

5

10 15

Feed cost [$/GJ]

20

25

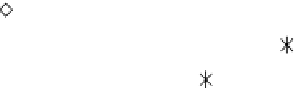

FIGure 12.2

Feed and processing cost of transportation fuels derived from lignocellulose and fossil

resources. (Reprinted from Lange, J.P.,

Biofuels Bioprod Biorefi,

, 1, 39-48, 2007. With permission.)

Wyman (1999) calculated that a 2.2 × 10

8

-L/year processing plant would cost $250 × 10

6

(1997

dollars). Third, the technology and processes (both biochemical and thermochemical) involved in

creating ethanol from various feedstocks are still immature and are being actively researched (Ruth

2008; Solomon et al. 2009). This can be seen in Figure 12.2, which shows the relative costs of feed-

stocks and processing for various transportation fuels. Access to capital investment and the need to

create transportation and market infrastructures are other challenges that will need to be overcome

for cellulosic ethanol to be commercially viable in large quantities.

The United States is the second-largest biodiesel producer in the world, behind Germany (Canakci

and Sanli 2008). In the United States, biodiesel is made primarily from soybeans. The U.S. industry

experienced rapid growth, expanding from 1.9 × 10

6

L produced in 1999 to 2.65 × 10

7

L in 2008

(NBB 2009). Production plummeted in 2009-2010 due to the recession, but has since rebounded

because of the RFS. The major cost of biodiesel is the cost of the feedstock, which accounts for

nearly 90% of the total fuel cost (Haas et al. 2005). Because the feedstock costs alone can be 1.5-3.0

higher than the price of diesel fuel, only lower feedstock costs or higher diesel prices will make

biofuels a more attractive option. The prices of plant-based feedstocks such as soybeans, canola, sun-

flower, and rapeseed are typically more expensive than various animal fats (Canakci and Sanli 2008).

12.3.2 E

uropEan

u

nion

The EU is the world's leading biodiesel producer, with approximately two-thirds of the world's mar-

ket (REN21 2009). Unlike the United States, biodiesel is the primary biofuel produced in the EU;

biodiesel makes up approximately 80% of the total biofuels produced in the region (Bozbas 2008).

Germany is by far the largest producer, producing half of all production. France, Italy, Spain, and

Austria are the next three largest producers. In total, the EU has 241 plants with a total capacity of

16 × 10

9

L/year, suggesting strong growth in the next few years (EBB 2008; REN21 2009). On the

other hand, in 2009 Germany and the United Kingdom lowered their mandatory blend rate by 1 and

0.5%, respectively, for a year in response to market conditions (FAO 2009).

12.3.3 B

razil

Brazil is the world's second-largest ethanol producer and has recently started producing biodiesel as

well. Between 2006 and 2008 Brazil increased ethanol production from 18 × 10

9

to 27 × 10

9

L, and

there are now 400 ethanol mills and 60 biodiesel mills in operation (REN21 2009). A total of 4.2 × 10

6

ha of sugarcane is harvested yearly. One reason for this massive increase is that sugar prices have

been dropping, whereas ethanol prices have been increasing (Moreira 2009).