Information Technology Reference

In-Depth Information

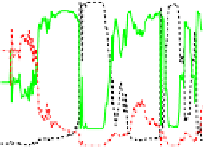

regime probability − online − low − 1189tac4

regime probability − online − mid − 1189tac4

regime probability − online − high − 1189tac4

1

1

1

O

B

S

O

S

O

B

S

0.8

0.8

0.8

0.6

0.6

0.6

0.4

0.4

0.4

0.2

0.2

0.2

0

0

0

0

20

40

60

80

100

120

140

160

180

200

220

0

20

40

60

80

100

120

140

160

180

200

220

0

20

40

60

80

100

120

140

160

180

200

220

Time in Days

Time in Days

Time in Days

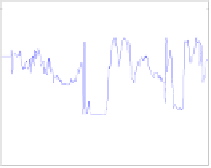

Fig. 9.

Game 1189@tac4 (Final TAC SCM 04) - Regime probabilities over time computed online

every day for the low (left), medium (middle) and high (right) market segment

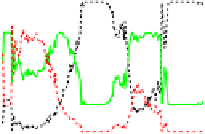

Entropy(Regimes) − low − 1189tac4

Entropy(Regimes) − mid − 1189tac4

Entropy(Regimes) − high − 1189tac4

1.5

1.5

1.5

1

1

1

0.5

0.5

0.5

0

0

0

0

50

100

150

200

0

50

100

150

200

0

50

100

150

200

Days

Days

Days

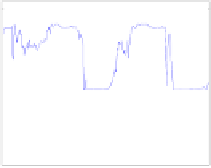

Fig. 10.

Game 1189@tac4 (Final TAC SCM 04) - Daily entropy values of the three regimes for

the low (left), medium (middle), and high (right) market segment

A measure of the confidence in the regime identification is the entropy of the set

S

of

probabilities of the regimes given the normalized mid-range price from the daily price

reports np

day

,where

S

=

{

P

(

R

1

|

np

day

)

,

···

,P

(

R

M

|

np

day

)

}

and

k

=1

−

M

Entropy(

S

)

≡

P

(

R

k

|

np

day

)log

2

P

(

R

k

|

np

day

)

.

(6)

An entropy value close to zero corresponds to a high confidence in the current regime

and an entropy value close to its maximum, i.e. for M regimes log

2

M

, indicates that

the current market situation is a mixture of

M

almost equally likely regimes. Examples

for the three market segments in game 1189@tac4 are shown in Figure 10.

5

Regime Prediction

The behavior of an agent should depend on the current market regime as well as expec-

tation of future regimes. This requires a way for the agent to predict future regimes and

when regime switches will occur.

We model regime prediction as a Markov process. We construct a Markov transition

matrix,

T

predict

(

r

t

+1

|

r

t

) off-line by a counting process over past games. This matrix