Environmental Engineering Reference

In-Depth Information

n

,

N

, with

n

the time index, successive

x

n

separated by a sampling interval

=

1, 2, 3,

...

1.0

(including units of

time), and

N

the number of observed data points. The

length of the time series is

T

δ

F

(

x

)

=

δ

. Here, we focus our

attentionondiscrete time series with values equally spaced

in time, recognizing that time series that are unequally

sampled or with few non-zero values unequally spaced,

also are com

m

on.

The

mean x

and

variance

N

0.5

f

(

x

)

x

of the time series values

x

n

taken over

N

values are given by:

σ

0.0

−

4

−

3

−

2

−

10

1234

N

N

1

N

1

x

x

)

2

x

(no units)

x

=

x

n

,

σ

=

(

x

n

−

(3.1)

N

−

1

n

=

1

n

=

1

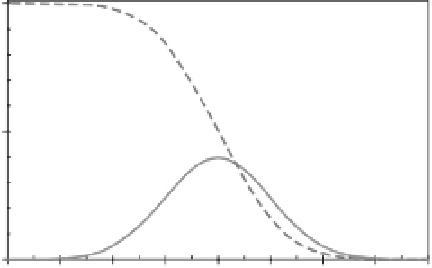

Figure 3.2

The probability distribution function

f

(

x

) (solid

line) and the cumulative distribution function

F

(

x

) (dashed

line) for the standa

rd

form of the Gaussian (normal)

distribution, mean

x

where

σ

x

is the standard deviation.

The discrete values

x

n

can be characterized by a con-

tinuous

frequency-size distribution f

(

x

), i.e., the relative

number of large, medium, and small values that are in the

time series. A widely applicable frequency-size distribu-

tion frequently used to model time series is the

Gaussian

(normal) distribution

. The probability density function

(pdf) for this distribution takes the form:

=

.

σ

x

=

.

0

0 and standard deviation

1

0,

from Equations 3.2 and 3.3.

the

k

th

moment is determined by taking a value in a

distribution, subtracting the mean, raising this to the

k

th

power, doing this again for all other values in the

distribution, summing the results, and properly normal-

izing. For some time series, higher moments can also

be specified, such as the

skewness

(third-order moment),

kurtosis

(fourth-order moment), and so on, to reflect the

lack of symmetry or spikiness of the distribution. For

the Gaussian distribution, these higher moments are zero

because of the symmetry and shape of the distribution. A

stationary time series

is one in which a given moment, if it

exists, is independent of the length of the interval within

a time series considered. If a given moment increases or

decreases as a function of the interval length, the time

series is

non-stationary. Weak stationarity

is where the

mean and the variance are approximately independent of

the length of the interval considered. In weak stationarity,

highermoments of the frequency-size distribution are not

considered.

Strong (strict) stationarity

is where the mean

and the variance, if they exist, do not change at all as a

function of length of the interval considered. Stationar-

ity will be discussed throughout this chapter, along with

examples, and will be assumed to be weak stationarity

unless indicated otherwise.

Another frequency-size distribution of interest for

modelling time series is the

Pareto distribution

.The

important aspect of this distribution is the frequency

of occurrence of large values decays as a

power law

of

the values. This behaviour contrasts with the Gaussian

distribution, which decays as an

exponential

of large val-

ues. This contrast is shown in Figure 3.3. The exponential

σ

x

exp

−

x

)

2

1

(

x

f

(

x

)

=

−

(3.2)

π

)

0

.

5

σ

x

(2

2

where

x

and

σ

x

are the mean and standard deviation of

the probability distribution and 'exp' is the exponential

function. The probability that the value

x

lies in the

range (

x

1

2

1

2

x

.In

addition to characterizing the

noncumulative probability

of a given value occurring at a given size (the pdf), one

can also characterize the

cumulative probability

of a value

occurring greater than or equal to (or less than or equal

to) a given size. A

cumulative distribution function

(cdf) is

obtained from the probability distribution (pdf) function

by the integration:

−

x

)to(

x

+

x

)isgivenby

f

(

x

)

∞

F

(

x

)

=

f

(

u

)d

u

(3.3)

x

In this case

F

(

x

) is the probability that a value

u

in the

distribution lies between

x

and infinity. The pdf and cdf

for the Gaussia

n

distribution are given in Figure 3.2 taking

a mean value

x

=

0 and a standard deviation

σ

x

=

1

.

0

(called the standard Gaussian distribution).

The Gaussian frequency-size distribution is a

symmet-

r

ic distribution

that is completely specified by its

m

ean

x

and its standard deviation

σ

x

. The quantities

x

and

x

are the first- and second-order statistical

moments

of

any distribution of time-series values. Different moments

described the shape of a statistical distribution, where

σ

Search WWH ::

Custom Search